KARACHI: A major incentive has been provided in the Federal Budget 2020-21 by prescribing reduced rates for certain imports.

A major change has been introduced with respect to rate of tax to be collected at import stage. In the past, all imports were subject to a standard rate of 5.5% except certain industries subjected to reduced rates.

Accordingly, there has always been a need to obtain certificates of exemption in case of import of items such as capital goods, raw materials, etc.

It appears that such reduced rates will be applicable for import of capital goods and raw materials.

Nevertheless, this classification is not apparent from the amendment made in the law whereby reduction in rate to 1% and 2% have been related to items imported irrespective of their eventual use.

For the purpose of collection of tax at import stage, all imports have been categorised as Part I, Part II and Part III of the Twelfth Schedule, wherein rate of WHT is 1.0% for imports under Part-I; rate of WHT is 2.0% for imports under Part-II; and rate of WHT is 5.5% for imports under Part-III.

The advance tax collected under section 148 in following cases is now also proposed to be minimum tax on income of the importer in all cases:

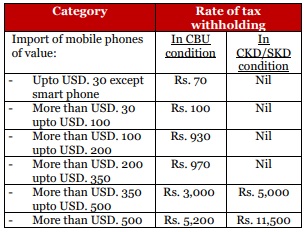

– Motor vehicles in CBU condition by manufacturers of motor vehicles;

– Large import houses;

– Foreign produced film imported for the purposes of screening and viewing.

The advance tax collected under section 148 for import of capital goods and raw material by an industrial undertaking for its own use will not be treated as minimum tax.

The classification of capital goods and raw material relates to the activity to be undertaken by the taxpayer. As stated above, this incidence may not commensurate with the incidence at the import stage where goods are classified in a different manner under the HS code.

Moreover, rate of WHT is proposed to be 1.0 percent on all imports by manufacturers covered under rescinded SRO 1125. Rate of WHT is proposed to be 4.0 percent on import of finished pharmaceutical products that are not manufactured otherwise in Pakistan, as certified by the Drug Regulatory Authority of Pakistan (DRAP).

A consequential amendment is proposed in other provisions whereby exemption certificate can now only be issued for import of plant & machinery.

Limiting the exemption certificate for import of plant & machinery only is not practically possible in all cases if 2% withholding on imports is mandatorily required on import of items in Part II of the Twelfth Schedule.